Professional liability insurance (also known as errors and omissions insurance) protects anyone providing professional advice or services, including law firms, consultants, and contractors, from the financial fallout of mistakes or alleged misrepresentations. If a client claims your services caused them harm or loss, this coverage helps cover the associated costs.

If you're running a law firm, you've probably worried about lawsuits at some point. Claims can pop up out of nowhere, and defending them gets expensive quickly. Even with an insurance policy in hand, one of the biggest fears when a claim hits is the immediate out-of-pocket cost.

That’s where a feature called First Dollar Defense comes into play, an option that can save you from the upfront expenses of a lawsuit. Let's explore what first dollar defense is, how it works, and whether it's worth the investment for your firm.

What Is First Dollar Defense?

First Dollar defense (FDD), sometimes called a “Loss Only Deductible”, is a feature in professional liability insurance coverage that covers legal defense costs from the moment a claim is filed, without requiring the insured to pay the deductible first.

The term "first dollar" means the insurance company begins paying for the defense expenses, such as attorney fees, court costs, and investigations, from the very first dollar spent. The policyholder only pays their deductible if the claim results in a settlement or judgment (an indemnity payment).

How Does First Dollar Defense Work?

The process is straightforward, and understanding how it works shows why it can be a valuable protection for your practice.

When a claim or lawsuit is filed against you, you notify your insurance carrier. With First Dollar Defense coverage, your insurer begins paying for your legal defense right away. This helps you avoid the upfront cost of a potentially large deductible just to get the legal defense process started.

If the claim is dismissed or resolved with no payout to the claimant, you owe nothing toward your deductible. However, if there’s a settlement or judgment, your deductible applies only to that payment (the indemnity amount).

For example:

A client files a malpractice claim against your firm for $200,000. Your policy has a $5,000 deductible and $1 million coverage limit.

- Without first dollar defense - You pay the first $5,000 in legal fees before your insurance begins to cover costs.

- With first dollar defense - Your insurer pays all defense expenses from the start, say, $70,000 in attorney and court fees, while your full $1 million limit remains available for any settlement or judgment. You pay nothing upfront unless the claim results in a payout.

First Dollar Defense Coverage vs. Traditional Deductible Coverage

First Dollar Defense (FDD) pays for legal defense costs from the moment a claim is filed, without requiring any deductible to be met first. You pay nothing out of pocket for defense unless the claim results in a settlement or judgment.

Traditional Deductible Coverage requires the insured to pay a set deductible before the insurance kicks in. All defense costs must be covered out of pocket until the deductible is satisfied.

The main difference: First dollar defense provides immediate financial relief with no upfront costs, while traditional deductible coverage requires the policyholder to pay initial expenses before insurance benefits apply.

What Are the Advantages and Disadvantages?

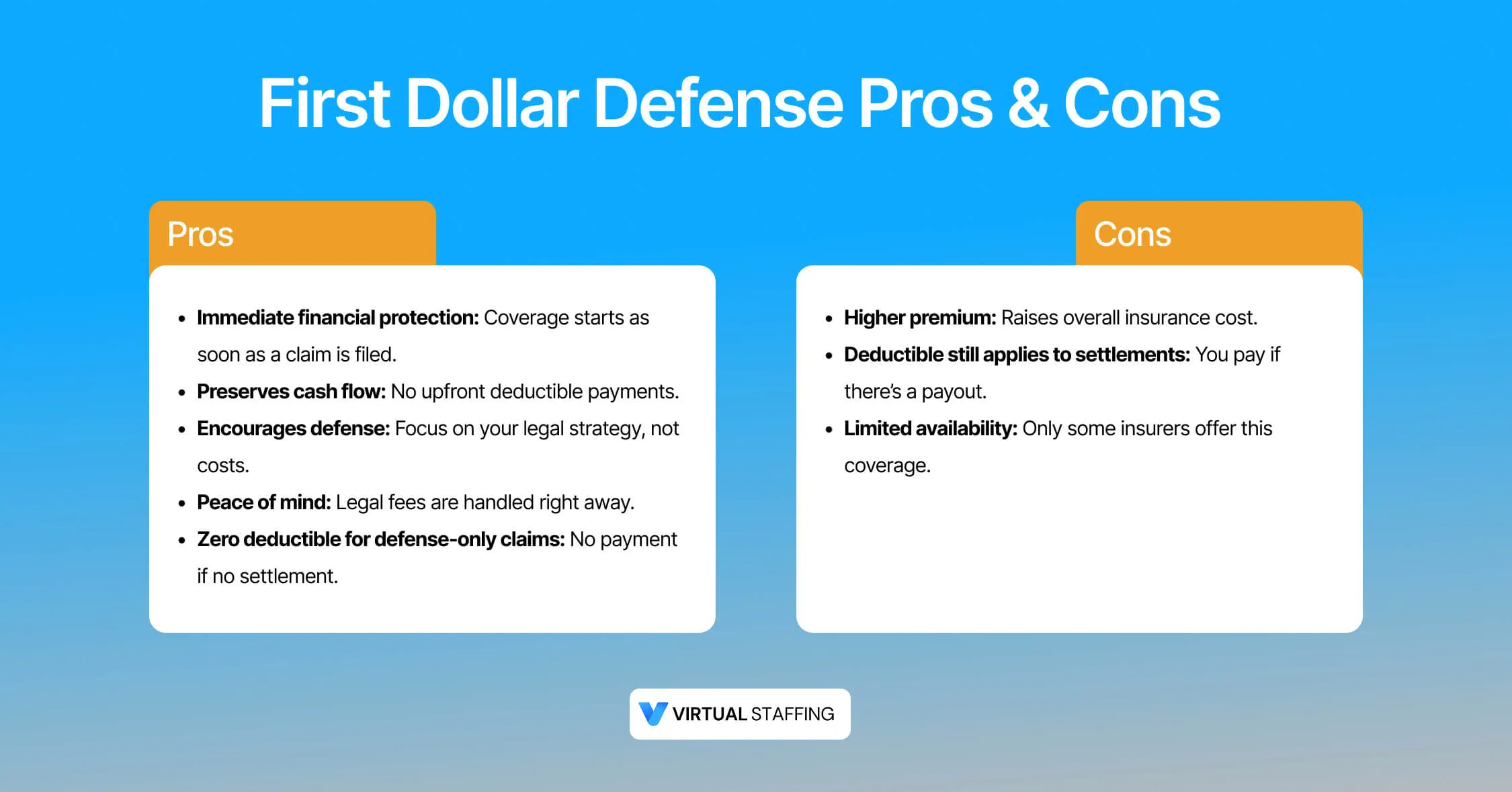

Pros

- Immediate financial protection. You're covered from the moment a claim is filed, with no out-of-pocket expenses for defense costs.

- Preserves cash flow. You avoid a sudden deductible payment that can be disruptive to your business operating finances.

- Encourages defense: You can focus on building the best strategy without worrying about mounting expenses.

- Peace of mind: Since legal expenses are handled immediately, it allows you to focus on your practice

- Zero deductible for defense-only claims. If the claim is dismissed or resolved with no indemnity payment, you pay nothing.

Cons

- Higher premium. Policies with first dollar defense increase your base professional liability insurance cost.

- Deductible still applies to settlements. If the insurer pays a settlement or judgment, you are responsible for your deductible

- Limited availability. Not all insurers offer FDD, and some restrict it to certain practice areas or specific policy structures.

When Do You Need First Dollar Defense?

For many law firms, the decision depends on their financial position, practice area, and risk exposure. You may consider first dollar defense if:

- You practice in high-risk areas like personal injury, real estate, or estate planning, where malpractice claims are more frequent

- Your firm operates on tight cash flow and can't easily absorb unexpected legal defense costs

- You want to avoid upfront expenses when a claim is reported

- You value the peace of mind of having your defense costs immediately covered

- You're in the early years of practice and are still building your financial reserves

- You've faced claims in the past and understand how quickly defense costs can accumulate

How Much Does First Dollar Defense Cost?

The cost of adding first dollar defense to your insurance coverage is not fixed. It varies based on factors such as the size of your deductible, jurisdiction, practice area, and claims history. Typically, you can expect to pay an additional cost as it increases your insurance premium.

It’s always best to consult your insurance agent for a precise quote. If you currently pay a deductible on your policy, compare your annual deductible expenses with the additional premium for FDD. In many cases, the financial protection and peace of mind can outweigh the added cost, especially if you practice in areas with higher claim frequency.

Final Notes

For many attorneys, first dollar defense provides enhanced protection and peace of mind that makes the additional premium worthwhile. It shifts the immediate burden of legal defense from your shoulders to your insurer. With an FDD policy, you can focus on growing your practice without constant worry.

Before making your decision, take time to assess your practice's needs, review your finances for unexpected expenses, and get quotes from multiple insurers to compare both coverage options and costs.

If you need support with selecting the right coverage or handling documentation, Virtual Staffing offers virtual assistants for law firms that can help streamline the process and ensure everything is properly managed.

This information is provided for general informational purposes only and is not intended as legal advice.